How to Read SEC Filings During a Geopolitical Shock

When a geopolitical headline breaks — a Taiwan strait incident, a new round of export controls, a chokepoint at sea — the standard investor response is to pull up CNBC and wait for someone to tell them what to do.

There is a better move. Every publicly traded company that has material exposure to that risk has already written it down, signed it, and filed it with the SEC. The question is knowing which paragraph to find.

We built a supply chain graph from 557 real filing edges — supplier and customer relationships extracted directly from 10-K and 20-F filings, not from news articles. Then we mapped the 10 companies with the highest geopolitical exposure and the richest SEC data, and traced the chokepoints they share.

Here is what we found.

The Right Way to Read a 10-K During a Crisis

Most investors jump to Item 1A — Risk Factors. That is the wrong place to start. Risk Factors is the legal laundry list: every company in the semiconductor space mentions geopolitical risk, Taiwan, and export controls. It is written to be comprehensive, not useful.

Start with Item 1 (Business). That is where companies describe what they actually do — which foundry they use, which customers they depend on, which suppliers make a product that no one else makes. The risk becomes real when you match the Item 1A warning to the named counterparty in Item 1.

The three words to search for when a shock hits: "foundry", "sole supplier", "concentration". When you find them in Item 1, you have found the exposure.

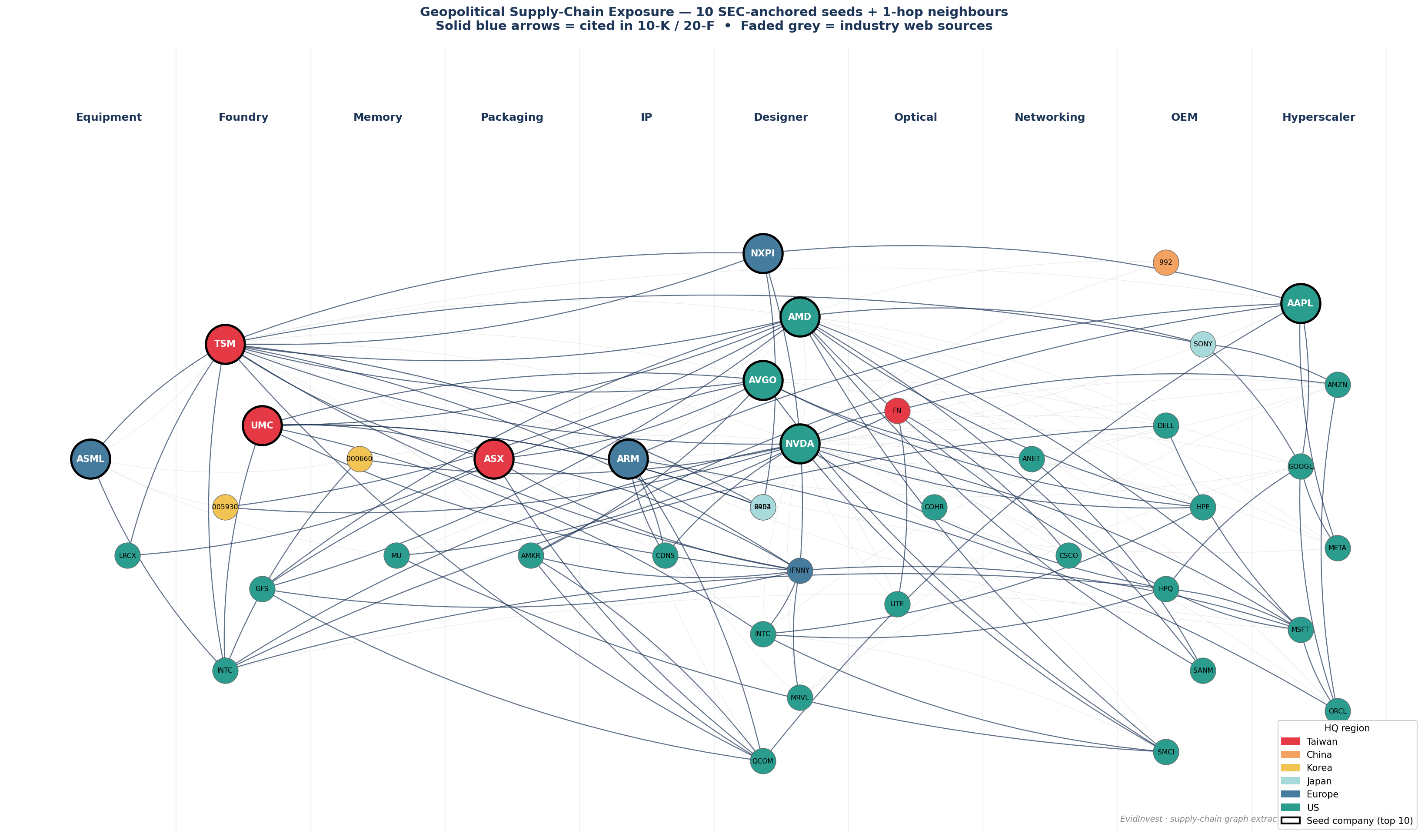

The Supply Chain Graph

We extracted 557 supplier/customer relationships from 10-K and 20-F filings across 365 companies in the datacenter and semiconductor ecosystem. The visualization below shows the 10 highest-exposure seed companies and the 31 hubs that connect at least two of them — 41 nodes, 170 edges, every one anchored to a real SEC filing.

Solid arrows = SEC-cited supplier/customer edges (10-K / 20-F). Faded arrows = curated industry sources. Node size = degree centrality.

Four chokepoints dominate this graph. Here they are, in order of how many seeds they can disrupt simultaneously.

Chokepoint 1: TSMC — The One Nobody Can Route Around

Open the filing for almost any US chip designer and search "TSMC." You will find it in Item 1, not buried in Risk Factors.

NVIDIA 10-K (acc. 0001045810-26-000021):

"We utilize foundries, such as Taiwan Semiconductor Manufacturing Company Limited, or TSMC, and Samsung Electronics Co., Ltd., or Samsung, to produce our semiconductor wafers."

AMD 10-K (acc. 0000002488-26-000018):

"We rely on Taiwan Semiconductor Manufacturing Company Limited (TSMC) for the production of all wafers for microprocessor and GPU products at 7 nanometer (nm) or smaller nodes."

Broadcom 10-K (acc. 0001730168-25-000121):

"During fiscal year 2025, approximately 95% of the wafers manufactured by our CMs were produced by TSMC."

Intel 10-K:

"Some of our most advanced current and future products are or will be either exclusively manufactured by TSMC or reliant upon critical components, including various compute die, manufactured by TSMC."

NVIDIA alone accounts for roughly 22% of TSMC's 2026 revenue — approximately $33 billion. Apple accounts for another 18%. NVIDIA also takes approximately 60% of TSMC's CoWoS advanced-packaging capacity. Eight of the ten companies in our graph have a direct filing-cited edge to TSM.

There is no short-term alternative. Samsung Foundry and Intel Foundry Services both exist, but neither has TSMC's advanced-node yield at scale for 3nm and 5nm logic. A Taiwan strait disruption that affects TSMC is not a supply chain risk — it is a supply chain stop.

Explore the data: TSMC financials | TSMC growth rates | TSMC valuation

Chokepoint 2: ASML and Carl Zeiss — The Chokepoint Behind the Chokepoint

TSMC cannot make leading-edge chips without ASML's EUV lithography machines. And ASML cannot make EUV machines without one specific company in Oberkochen, Germany.

Intel 10-K:

"ASML Holding N.V. (ASML) is currently the sole supplier of EUV lithography tools that we are deploying in our Intel 4, Intel 3, Intel 18A and planned future leading-edge manufacturing nodes."

ASML 20-F:

"The number of lithography systems we are able to produce is limited by the production capacity of one of our key suppliers, Carl Zeiss SMT, our sole supplier of lenses, mirrors, illuminators, collectors and other critical optical components."

Two companies. Both in NATO countries (Netherlands and Germany). A disruption to either one does not slow leading-edge chip production — it stops it globally. There is no second source for EUV optics and no second source for EUV machines. ASML shipped 44 EUV systems in 2024 and cannot materially accelerate that number.

This is the paragraph most investors skip. It is the most important one in the entire semiconductor supply chain.

Explore the data: ASML financials | ASML growth rates | ASML valuation

Chokepoint 3: The Taiwan Substrate Cluster — The Story Nobody Tells

Every AI chip that TSMC packages using CoWoS technology depends on two material inputs that almost no financial analyst covers.

The first is Ajinomoto Build-up Film (ABF) — a substrate material with exactly one producer in the world: Ajinomoto, the Japanese food and chemical company. ASE Technology's 20-F names it directly:

"The Ajinomoto Build-up Film (ABF) substrate, a crucial component for manufacturing high-performance chips, may face a higher risk of supply shortages or extended lead times due to potential strong demand for AI."

The second is the IC substrate cluster — Kinsus, Nan Ya PCB, and Unimicron — all headquartered in Taiwan, all in our graph as second-hop nodes from NVIDIA and Broadcom. These companies produce the package substrates that sit between the chip die and the PCB in every high-end processor.

The chain for a single NVIDIA H200 looks like this:

NVIDIA design → TSMC fabrication (Taiwan) → ASE Technology packaging (Taiwan) → Ajinomoto ABF (Japan) → Unimicron substrate (Taiwan)

Every link in that chain except the design step runs through Taiwan or a sole-supplier Japanese firm. A logistics disruption — not even a military one — can cascade through all of them simultaneously.

Explore the data: NVIDIA financials | NVIDIA growth rates | NVIDIA valuation | Broadcom financials

Chokepoint 4: NVIDIA's Export Control Treadmill

No filing in the semiconductor sector covers geopolitical risk more precisely than NVIDIA's 10-K. They have been living inside the export control regime for three years and have documented every iteration.

"Over the past three years, we have been subject to a series of shifting and expanding export control restrictions… In April 2025, the USG informed us that it requires a license for export to China (including Hong Kong and Macau) and D:5 countries, or to companies headquartered or with an ultimate parent therein, of our H20 integrated circuits and any other circuits achieving the H20's memory bandwidth, interconnect bandwidth, or combination thereof."

The sequence: A100/H100 ban (October 2022) → H800/A800 China-specific SKUs (late 2022) → second restriction extending to Country Group D:5 covering Saudi Arabia, UAE, Vietnam (October 2023) → H20 ban (April 2025).

The pattern matters as much as the current rule. NVIDIA engineered around each prior restriction — the H800 was built specifically to comply with the 2022 rules — and the H20 ban landed after they had already invested in that workaround. The D:5 extension shows the scope expanding beyond China into Gulf states that are building out massive AI datacenters.

The investor question here is not "what are the current rules" — it is "how quickly does the rule set change and how much revenue is at risk each time." NVIDIA's 10-K answers that directly. Most investors have not read it.

Chokepoint 5: Arm China — The Governance Disclosure Most Readers Skip

One more filing is worth your attention. ARM's annual report contains a disclosure that does not appear in news coverage:

"Our concentration of revenue from the People's Republic of China… makes us particularly susceptible to economic and political risks affecting the PRC… We utilize our commercial relationship with Arm Technology (China) Co.… Neither we nor SoftBank Group control the operations of Arm China, which operates independently of us."

Arm China is ARM's single largest customer, representing approximately 24% of FY2025 revenue. ARM has disclosed in writing that it does not control the entity that licenses its IP inside China. That entity operates independently of both ARM and SoftBank.

This is the kind of paragraph that does not move a stock until a headline forces it to. It is sitting in the filing right now.

Explore the data: ARM financials | ARM growth rates | ARM valuation

The Chokepoint Scoreboard

| Chokepoint | HQ | Seeds exposed | Why it matters |

|---|---|---|---|

| TSMC | Taiwan | 8 of 10 | Only source of ≥7nm logic at scale. No short-term substitute. |

| ASML | Netherlands | 5 of 10 | Sole EUV supplier globally. No EUV = no leading-edge node. |

| Carl Zeiss SMT | Germany | 5 of 10 | Sole optics supplier to ASML. The chokepoint behind the chokepoint. |

| ASE Technology | Taiwan | 4 of 10 | Largest OSAT; CoWoS overflow capacity for NVIDIA. Taiwan-substrate dependent. |

| Ajinomoto (ABF) | Japan | 4 of 10 | Sole supplier of advanced-packaging build-up film worldwide. |

| SK Hynix | South Korea | 2 of 10 | Primary HBM3/HBM4 supplier for AI training chips (NVIDIA, AMD). |

| Arm China | China (independent) | 1 of 10 | 24% of ARM revenue, not controlled by ARM or SoftBank. Disclosed in 20-F. |

What This Means for Investors

The standard geopolitical analysis asks: "what happens if Taiwan gets blockaded?" That is the right question but the wrong level of resolution.

The better questions — the ones you can actually answer from public filings — are:

Which specific counterparty does this company name in Item 1? AMD writes "all wafers at 7nm or smaller." That is not a risk factor disclosure. That is an operational dependency. The company has told you exactly what breaks.

How many seeds does this chokepoint touch? TSMC disrupts eight of our ten seed companies simultaneously. Ajinomoto disrupts four. Carl Zeiss disrupts five through ASML. A shock that hits one of the top three chokepoints is not a sector rotation — it is a systemic event.

Is there a secondary disclosure you have not read? The Arm China governance disclosure, the NVIDIA H20 export sequence, the ASE 20-F on ABF shortages — these are all in public filings. They are not secret. They are just unread.

The reason most geopolitical analysis is generic is that analysts read news instead of filings. When you read the filings, the supply chain stops being abstract. It becomes a named company in a named location with a named customer who has already quantified the dependency in a signed document.

Explore the Data

Every supplier/customer relationship in this post is extracted from public SEC and 20-F filings in the EvidInvest database. You can trace the same edges, read the source documents, and run valuation models on any company in the graph.

- NVIDIA — AMD — Broadcom — TSMC

- ASML — ARM — NXP — Apple

- SEC-backed intelligence: Explore the source-cited findings in the AI datacenter report or sample report while the filing-level viewer is prepared for release.

- Growth rates: Compare revenue and earnings trajectories across NVDA, TSMC, ASML

- DCF valuation: Model fair value for NVDA, ASML, ARM

Subscribe to get the next post in the series — we are working through the second-order chokepoints: HBM memory concentration, advanced packaging capacity, and the OSAT geography problem.

Supply chain data sourced from 557 filing-cited edges across 365 companies, extracted from 10-K and 20-F filings in the EvidInvest SEC database as of May 2026. Quotes are verbatim from public filings. This is not investment advice — always do your own due diligence.

Fair Value Weekly

Get DCF breakdowns, fair value updates, and portfolio ideas for serious investors. No spam, no paywalled teasers.